Why Late-Stage Companies Are Waiting Until 2026 to IPO

If you've been watching the IPO market, you might have noticed something strange: despite signs of rebounding public markets, tech IPOs are getting pushed back. Companies that were rumored to go public in 2023 aimed for 2024, then 2025, and now are quietly targeting 2026.

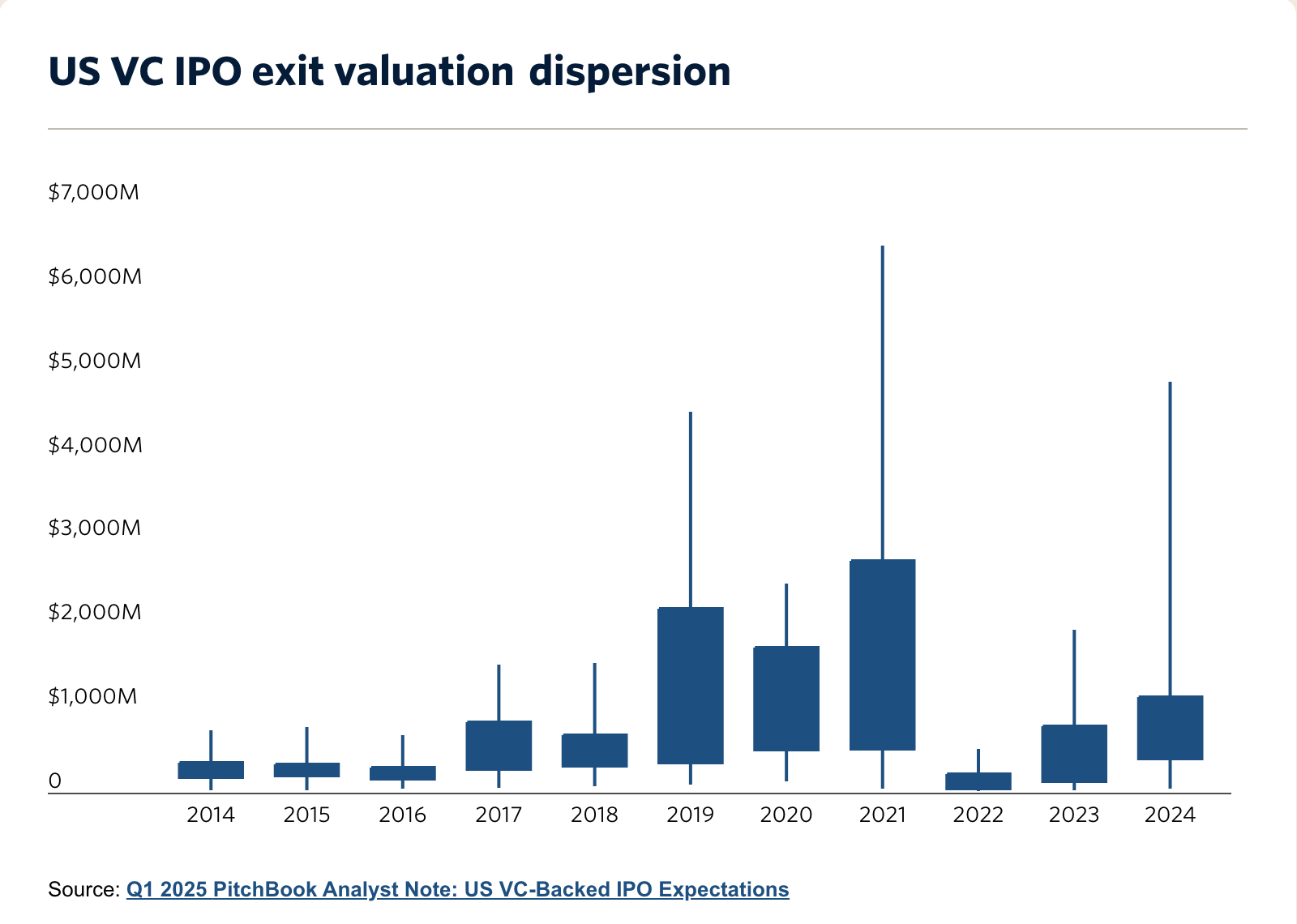

This isn't just speculation. The data tells the story. After the 2021 IPO bonanza (when nearly 400 companies went public), we've seen a dramatic slowdown. Only 154 IPOs raised $19.4 billion in 2023, and 2024 wasn't much better, with just 42 venture-backed companies taking the plunge. Even with the S&P 500 soaring 23.3% in 2024, late-stage private companies largely stayed on the sidelines.

So why the hesitation?

The answer isn't simple, but it's becoming clearer. A perfect storm of factors—interest rates, new tariff policies, market volatility, valuation mismatches, and strategic positioning—all coming together to make 2026 look like a better window for companies to finally make their public debut.

In this analysis, we’ll break down some of the latest data to explain why we're seeing this calculated patience from late-stage companies.

The Current IPO Landscape

At first glance, the IPO market appears to be recovering. We've seen a 45% increase in IPO proceeds and 40% more IPOs in 2024 compared to the dismal 2023 numbers. Public markets were strong in 2024, with the S&P 500 gaining 23.3% and continued its upward trend into Q1 2025.

But dig a little deeper, and the picture is more nuanced.

While there were encouraging signs, we're nowhere near the robust pre-pandemic IPO environment. Only 42 venture-backed companies completed IPOs in 2024—the lowest number for non-healthcare tech IPOs since 2011. Compare that to the historical average of around 75 IPOs annually (excluding 2021), and it's clear the market is constrained.

The interest rate environment also tells part of the story. The Fed has begun its cutting cycle, with 75 basis points of easing projected for 2025, but rates are still much higher than during the zero-interest-rate era that fueled the 2021 IPO boom.

For the IPOs that did happen in 2024, performance has been mixed but encouraging: 85% priced within or above their expected range, and post-IPO performance averaged above 20%. Reddit stands out as a notable success, trading at a market cap over $30 billion after going public at just over $5 billion.

However, companies like Tempus AI and Pony.ai went public at valuations 50% lower than their private market peaks—a valuation haircut many late-stage companies don’t want to accept (understandably).

The reality is clear: despite some improvements, we're still looking at an annual IPO proceeds figure far below the pre-2020 average of $45 billion. For most late-stage companies, the current environment just doesn't offer the right conditions for a solid public debut.

Macroeconomic Factors Favoring 2026

So why wait until 2026? Lets break the big reasons down one by one.

The Valuation Gap Problem

The biggest factor deterring IPOs is straightforward: companies face devastating valuation cuts when going public in the current environment.

The data is striking: half of the non-healthcare unicorn IPOs in 2024 were completed at lower valuations than their prior VC financing. Even Reddit, often cited as a success story, went public at a valuation 50% lower than its private peak.

In 2023, two out of three non-healthcare unicorn IPOs faced similar valuation haircuts. These aren't minor adjustments—they represent billions in lost value for founders, employees, and investors.

By waiting until 2026, companies are betting (or hoping) the valuation gap will narrow as interest rates stabilize and market conditions improve.

The Profitability Mandate

The "growth-at-all-costs" era is definitively over. Public investors have shifted their expectations, demanding clear paths to profitability rather than just impressive revenue growth.

This shift is quantifiable: EV/EBITDA multiples at exit for VC tech IPOs have plummeted from their 2021 peaks of 46.2x to just 15.5x in 2024. Companies with negative EBITDA face even harsher reception.

Most late-stage companies built their business models during the zero-interest-rate era, optimizing for growth over profitability. They now need time to restructure operations, which explains why 2026 has emerged as the target—it provides the runway needed to demonstrate sustainable profitability metrics.

Market Volatility and Geopolitical Uncertainty

It’s predicted market volatility won't return to favorable levels until the end of 2025, with valuations improving only in Q1 2026. The introduction of new tariff policies is also a major source of this.

PitchBook's European VC report states that "the curtains are closing on an IPO window in 2025" with forecasts pointing to 2026 as the next clear opportunity.

This timing aligns with interest rate projections as well. Despite modest cuts, rates will remain significantly higher than the zero-interest era through 2025.

The Crowded Pipeline

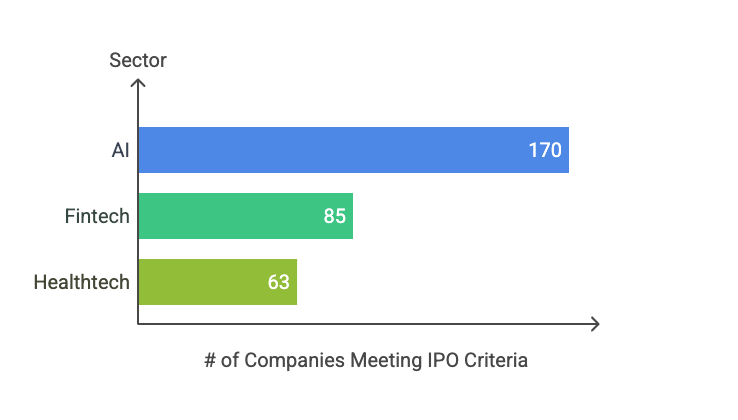

The sheer volume of IPO-ready companies has created unprecedented congestion. The 601 US companies that now meet IPO criteria (more than double the 288 in 2021) represent a staggering $1.5 trillion in private market value.

This crowding is particularly acute in high-growth sectors:

170 AI companies now fit IPO criteria (2.4x from three years ago)

85 fintech companies (up from 36)

63 healthtech companies (up from 16)

With so many companies competing for investor attention, going public now means fighting for oxygen in an already crowded space. Companies are strategically waiting for 2026 when market conditions should better support this volume of listings.

Who's Waiting for 2026? Some of the Big Names in the Pipeline

Let's look at some of the big names that signaled they're targeting 2026 for their public debuts.

Databricks

Databricks, valued at $55 billion (up from $43 billion in previous rounds), has been on IPO watch lists for years. But instead of rushing to market, they've taken a strategic approach. The company recently raised cash specifically to handle RSUs (restricted stock units) that are expiring in 2026—a clear sign of when they're planning their public entry.

Deel

Deel, the payroll and compliance platform valued at $12.6 billion, is another. CEO Alex Bouaziz has publicly indicated this timeline, noting that the company wants to build more predictable revenue streams and unit economics before facing public market scrutiny. With strong growth in international markets, Deel is using this time to cement its leadership position in their space.

Oyo

Oyo, the Indian hospitality chain, is particularly interesting. After withdrawing IPO filings in both 2021 and 2023, the company is now targeting March 2026 for its third attempt at a $7 billion valuation. This pattern of multiple postponements shows how companies are becoming more discriminating about market timing.

Klarna

Klarna also recently delayed its listing, joining companies like StubHub that pushed back their timelines. After a significant valuation adjustment in 2022, Klarna has been rebuilding and strengthening its financial position before testing public markets.

What ties these companies together isn't just their size or success—it's their strategic patience. Rather than forcing an IPO in suboptimal conditions, they're using their private status to strengthen their positions, improve unit economics, and time the market for maximum valuation.

How Companies Are Preparing

With 2026 in their sights, late-stage companies aren't just sitting around—they're actively positioning themselves for successful public debuts. They're following what we might call the "2026 IPO Playbook," and it looks different from strategies of the past.

First, there's a heightened focus on IPO readiness fundamentals. Companies are investing in governance structures, financial reporting capabilities, and leadership teams that will stand up to public market scrutiny. This means building boards with public company experience, implementing SOX-compliant financial controls, and establishing robust investor relations functions—all before they file their S-1.

Financial metrics are getting a complete overhaul. Data shows that tech IPOs with positive EBITDA have become increasingly important indicators of post-IPO success. Companies are reengineering their financial profiles to demonstrate not just growth, but sustainable, profitable growth. The days of going public with nothing but a growth story are behind us.

Strategic timing has become more sophisticated too. Companies are looking to capitalize on "vents"—short periods of favorable market conditions. Some companies are preparing all their IPO documentation now so they can quickly take advantage of these windows when they appear, even if their primary target remains 2026.

M&A is also playing a bigger role in pre-IPO strategy. With valuations somewhat depressed, strong companies with cash reserves are using this time to make strategic acquisitions that fill product gaps or expand market reach. These acquisitions can strengthen their story before going public, potentially commanding higher multiples when they do list.

Perhaps most challenging is talent retention. With longer timelines to liquidity, keeping key employees engaged requires creativity. We're seeing companies implement partial liquidity programs, refresh equity grants with extended vesting schedules, and create special incentive programs tied to 2026 IPO targets.

The valuation reset is being addressed head-on. The median IPO valuations have declined significantly from 2021 peaks. Rather than fighting this reality, smart companies are proactively managing expectations with their employees and private investors, while structuring their operations to deliver the metrics that will command premium valuations in the new market reality.

By following this playbook, companies are doing more than just waiting for 2026—they're actively shaping themselves into the kind of businesses that will thrive as public companies when that date finally arrives.

The 2026 IPO Wave

When we look at all these factors together, 2026 is shaping up to be a pivotal year for tech IPOs. The forecast is clear: volatility metrics should return to favorable levels by the end of 2025, with valuations improving in Q1 2026—creating the first clear IPO window in years.

The potential volume of IPOs in 2026 could be significant. With 601 companies now meeting traditional IPO criteria (just in the US), the backlog has more than doubled since 2021. If even a quarter of these companies go public, we'd be looking at a historic surge in listings. 2026 could match the 10-year average of 75 IPOs annually (excluding the outlier year of 2021)—a massive improvement from recent years.

Companies that have exercised strategic patience may find themselves rewarded. Those who went public during the challenging 2022-2024 period often had to accept significant valuation haircuts. Most companies that waited will likely face a more receptive market in 2026, with potentially stronger valuations and less post-IPO volatility.

For investors, this timeline creates both challenges and opportunities. Limited partners in venture funds are feeling the pinch of delayed returns, with distribution yields at just 6.5%, well below historical averages. But this pressure may also create secondary market opportunities as some investors seek earlier liquidity.

The tech ecosystem itself is evolving through this extended private period. Companies are building more sustainable business models, focusing on profitability, and creating more mature governance structures. When they do go public in 2026, they'll likely be stronger, more resilient businesses than they would have been with a rushed timeline.

What's clear is that the IPO landscape has fundamentally changed. The path from startup to public company is longer, more methodical, and more demanding than it was just a few years ago. But for companies that can navigate this extended journey successfully, 2026 represents not just an exit, but an opportunity to debut as mature, well-positioned public companies in what could be a much more favorable market environment.