What AI Actually Changes About Venture Capital (and What It Doesn't)

Why sourcing, winning, validation, management, and exits are being rewritten and what founders and funds should do about it

A few years ago, a strong seed-stage company had five engineers and a working prototype. Today I see solo founders with shipped products, paying customers, and no employees.

Building got cheaper overnight but a lot of funds still operate like it didn’t.

Venture capital has always been an information game. You find the signal early, earn the founder’s trust, validate faster than the market, then help the company scale into an outcome.

AI doesn’t change the existence of that game, but the playing field has shifted so much that many funds (ours included), are rethinking how they operate at a fundamental level.

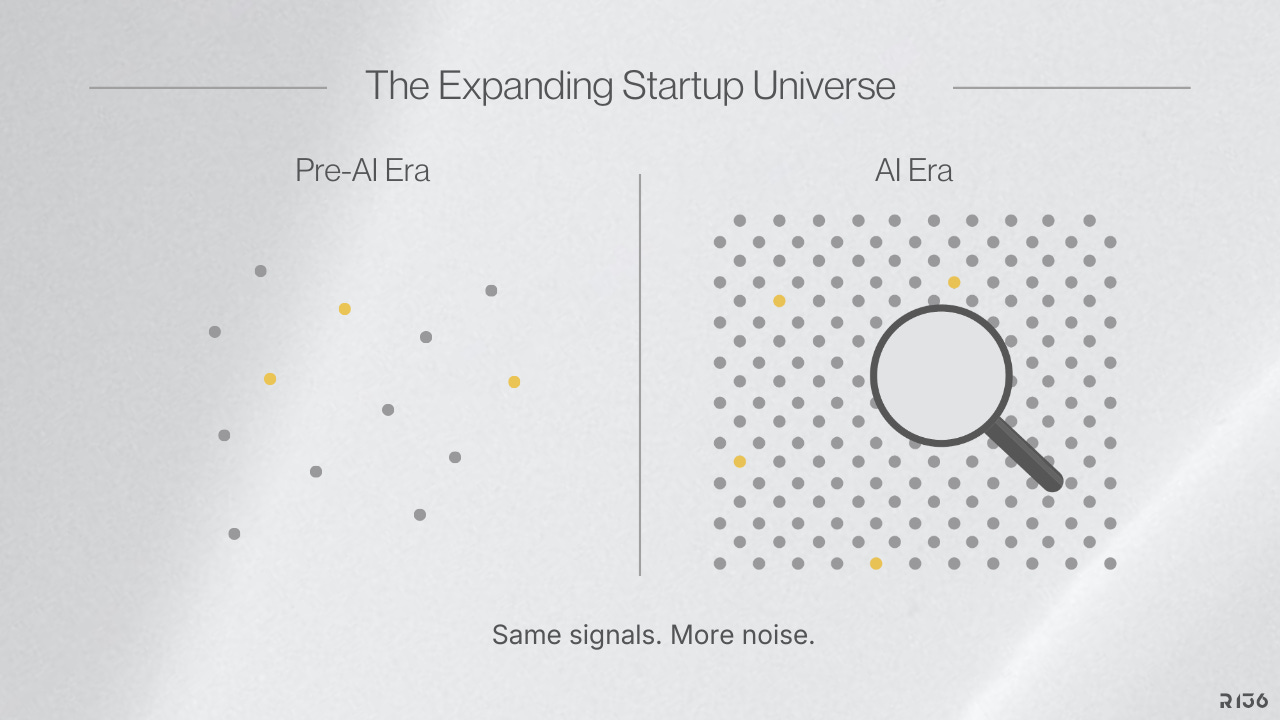

The reason is straightforward: when building gets cheaper and faster, more gets built. But when more gets built, there’s more noise. And when there’s more noise, the old playbook of warm intros, partner gut feel, and a few reference calls stops being enough.

I think about this through five pillars. Not because I love frameworks, but because these are the five jobs a fund actually does, and each one is under real pressure right now.

TL;DR

VC rests on five pillars: Sourcing, Winning, Validation, Management, Exit. All five are shifting.

AI massively increases the volume of startups and the speed of iteration, which means separating signal from noise is harder than it’s ever been.

Winning favors either massive generalists or sharply specialized funds. The middle is an uncomfortable place to sit.

Validation is deeper and faster, but also more necessary, because polished demos are now cheap to produce.

Management shifts toward helping AI-native teams stay lean, ship safely, and pivot without losing coherence.

Exit discipline matters more than ever when valuations can inflate well ahead of real adoption.

The Five Pillars of Venture Capital

Every venture fund, whether it says so or not, runs on five jobs:

Sourcing. Finding promising companies early.

Winning. Convincing the best founders to take your capital over someone else’s.

Validation. Deciding whether you truly want to invest once you’ve found something interesting.

Management. Supporting the company after the wire hits.

Exit. Reaching a liquidity outcome, whether that’s an acquisition, an IPO, or another path.

None of these are new. What’s new is the pressure AI puts on every single one of them, and how quickly that pressure is compounding.

What AI Changes, and What It Doesn’t

AI changes the cost of building, the speed of iteration, and the volume of data you can analyze, all at once. That combination expands the opportunity set considerably. It also expands the noise by the same factor, which is the part most people underestimate.

What doesn’t change is the need for judgment. Conviction. Trust. A clear view of where a market is heading, not where it sits today. I’ve watched tools improve every year for decades. But judgment has never once automated itself, and I don’t expect that to change anytime soon.

Pillar 1: Sourcing

Sourcing used to be a human-network game. Warm introductions, founder communities, a handful of visible accelerators, etc. Data existed, but analyzing it at scale wasn’t practical, so most funds relied on relationships and reputation to see deals early.

That world isn’t gone but it’s no longer enough. The startup universe is larger now. Teams are smaller but prototypes arrive faster.

I’ve seen companies reach meaningful revenue with three people, which is genuinely exciting, while also making the sourcing problem harder, not easier.

When anyone can build quickly, the question is no longer “who’s building?” It becomes “who’s building something defensible?” and that’s a fundamentally different kind of search.

Strong sourcing now requires model-assisted research across messy, fast-moving data: product launches, hiring signals, open-source momentum, community traction.

It also requires deep domain understanding, because knowing an industry’s real pain points matters as much as evaluating technical architecture. It requires access to networks and datasets that aren’t easily visible to the public.

And it requires tighter segment focus, because narrower geography, stage, and vertical yields sharper research and better differentiation.

Here’s a practical rule I keep coming back to: the wider your mandate, the more you need scalable systems to cover the ground. The narrower your mandate, the more you can rely on depth. But that depth has to be earned through sustained, real research. There’s no shortcut or substitute.

Pillar 2: Winning

Sourcing finds the opportunity. Winning secures it. These are two very different skills, and confusing them is one of the most common mistakes I see funds make.

If a company is exceptional, you’re almost never the only investor who noticed. By the time a strong founder is raising, they have options, and they’re evaluating you as carefully as you’re evaluating them.

Winning is the competitive layer of venture: brand, speed, terms, syndicate quality, and above all, whether the founder trusts you enough to pick up the phone at 11 PM when something breaks.

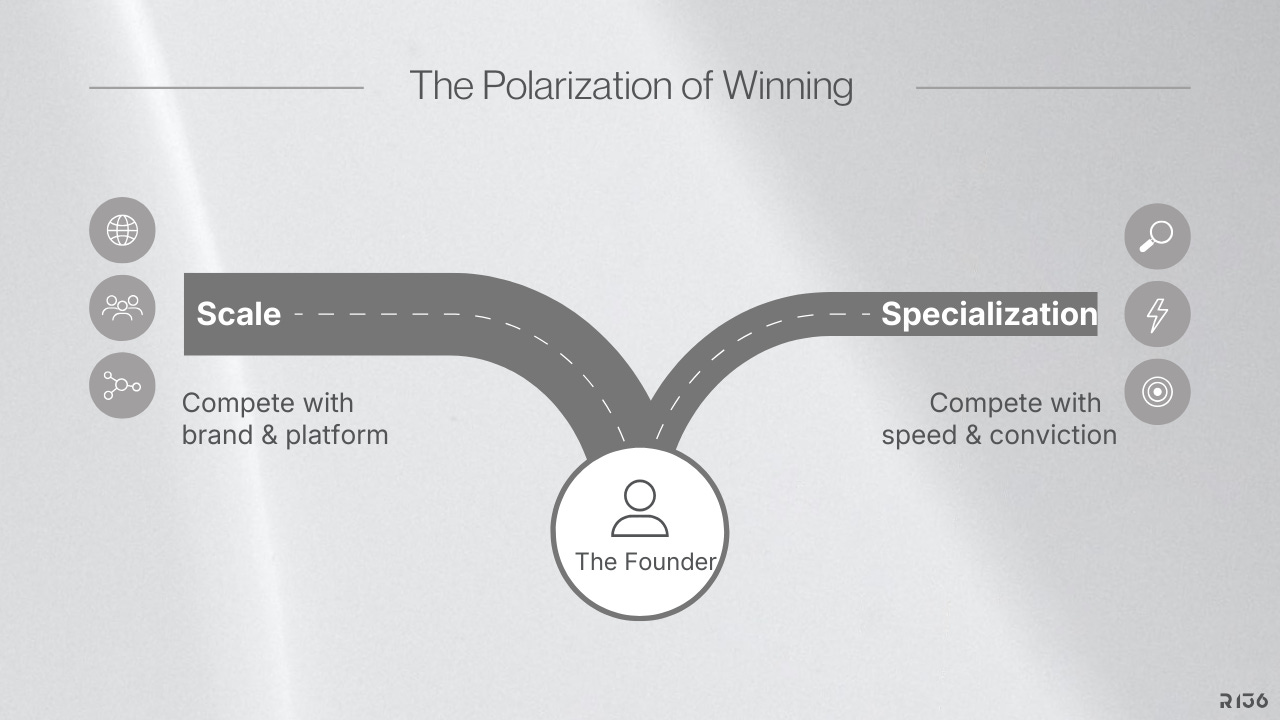

The market is polarizing in a way that’s hard to ignore. Large generalists compete with scale, platform support, and global reach, but that game requires enormous capital and infrastructure.

Smaller funds win through specialization, meaning a sharp thesis, fast decisions, and value that’s tangible inside a specific domain. When you already understand a founder’s problem before the first call, they notice. That’s what specialization actually earns you, and it compounds over time as your reputation within that segment grows.

The middle ground, where a fund has a broad mandate, modest capital, and generic value-add, is a difficult place to win from. And it’s getting more difficult every quarter as the poles pull further apart.

Pillar 3: Validation

Once a founder wants your capital, the job flips entirely. Now you have to decide if you really want to invest, and you have to make that decision with enough rigor to protect your fund while moving fast enough to not lose the deal.

This is where AI creates an interesting tension.

On one hand, research and analysis tools have improved dramatically, which means diligence can be deeper and faster than it was even two years ago. On the other hand, that same improvement in tools means a polished product demo isn’t proof of much anymore.

When you can build a compelling prototype in only a weekend, the demo tells you about ambition and taste, but not much about durability.

So the real questions have changed:

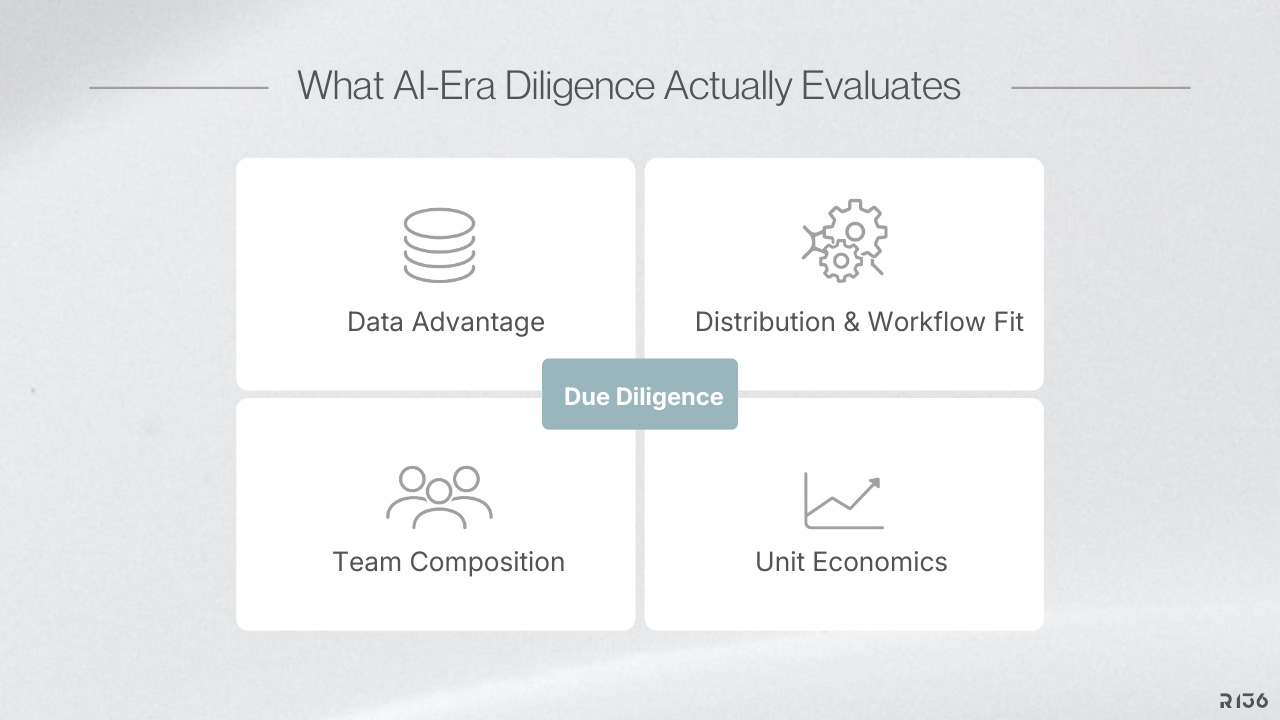

You need to understand data advantage: what proprietary or hard-to-access data makes this product better over time, and harder to replicate?

You need to understand distribution and workflow fit: where does this product sit in the real operating process of an enterprise, and does it replace an existing step or create a new dependency?

You need to evaluate team composition honestly: can a lean team ship reliably, handle security, and iterate without breaking things in production?

And you need to look hard at unit economics beyond the initial excitement, because the real test of a business comes when the novelty fades and the renewal conversation begins.

Diligence speed matters but depth matters more. The fastest “no” is still more valuable than a slow “yes” into the wrong company, and the discipline to walk away from something exciting but fragile is one of the hardest skills in this business.

Pillar 4: Management

After investment, a fund has to deliver on its promises. Things like helping the company hire the right people, building systems that scale, avoiding traps that are obvious in hindsight but invisible in the moment, and potentially raising follow-on capital when the timing is right.

The instinct with AI-native startups, especially for investors who came up in the previous era, is to impose familiar structure. More management layers. More process. More headcount.

I understand the instinct, because structure feels like progress, but with AI-native companies it’s usually wrong. The job is to help build a high-leverage organization that ships safely and scales with discipline, often with far fewer people than legacy playbooks assume.

I’ve watched a twelve-person AI company outperform a sixty-person competitor not because they had better individual talent, but because they designed their organization around leverage rather than headcount.

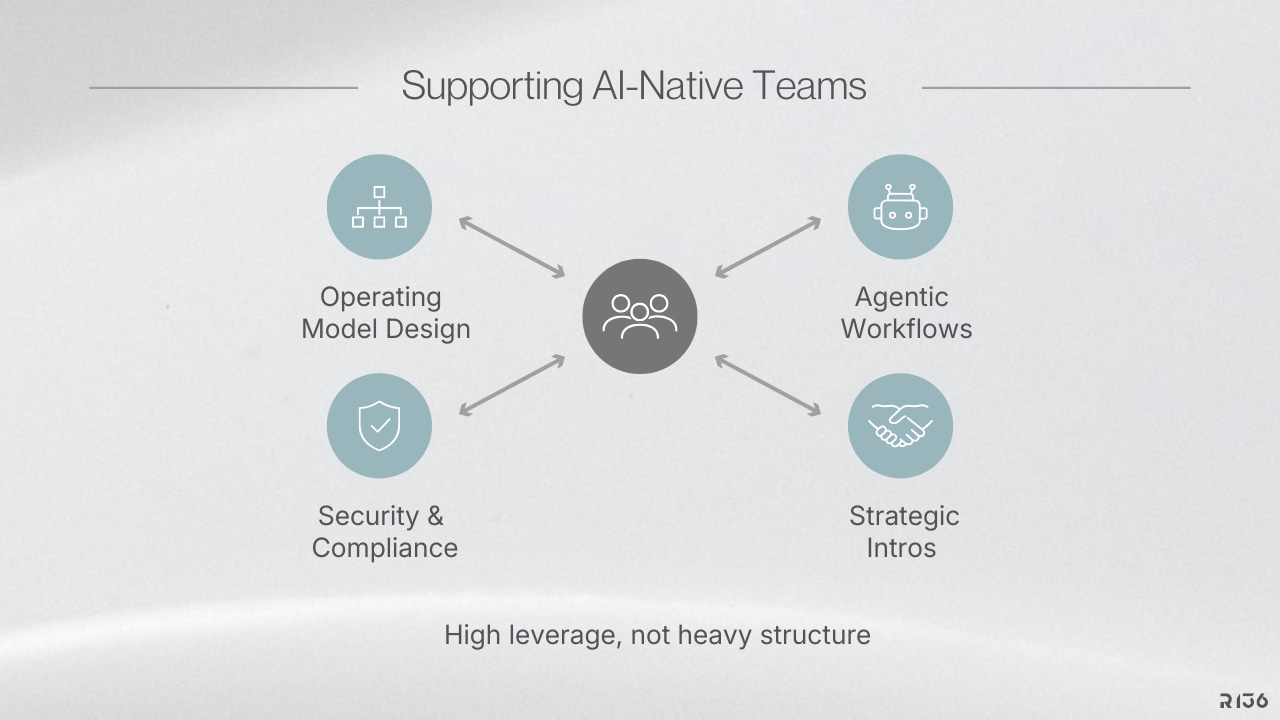

Where management support matters most is in operating model design for small teams. Things like decision cadence, ownership clarity, lightweight governance that doesn’t slow things down.

From there, it’s about helping teams adopt agentic and AI-assisted workflows that raise output per engineer rather than just adding bodies. Security, reliability, and compliance need to be built into the product early, not bolted on in a panic before a Series B.

And when the timing is right, the fund should be opening doors to the next layer of capital, customers, or distribution. Not too early and not too late.

The best portfolio companies don’t need hand-holding. They need a partner who’s seen the terrain before and can point out where the crevasses are, so they can move fast without falling in.

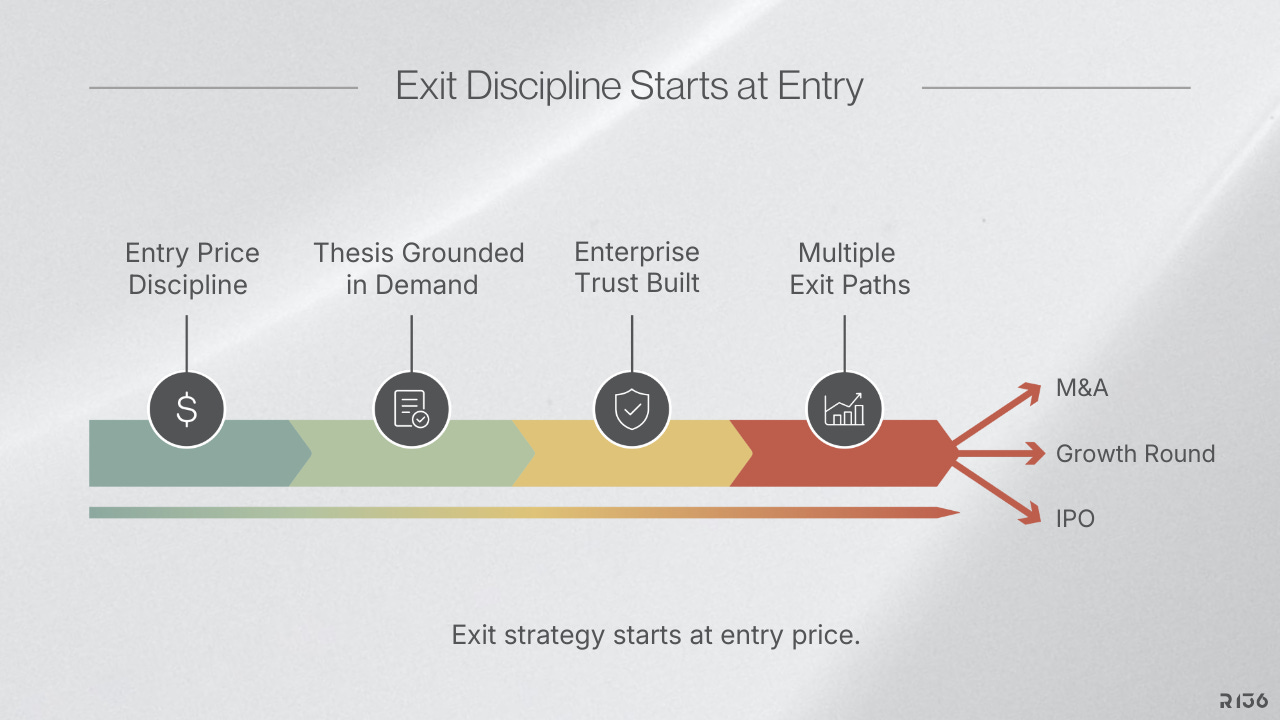

Pillar 5: Exit

Exit strategy starts at entry price. That was true twenty years ago and it’s still true now, but it’s remarkable how often this gets forgotten when markets heat up.

AI markets are particularly prone to valuation inflation, often well ahead of real, durable adoption. The cycle is familiar if you’ve been through a few of them.

A new technology captures attention, capital floods in, multiples expand on narrative rather than revenue quality, everyone finds a reason why this time the fundamentals don’t apply. And then, eventually, gravity reasserts itself.

For funds, the temptation is obvious: ride the wave, justify the price, assume the next round will validate the entry. A more robust approach, and the one I believe in, is to invest with a longer horizon in segments where AI’s impact is underappreciated and therefore underpriced.

These are the segments where strategic buyers will eventually pay for real capability rather than narrative, because they need what the company actually built.

Exit resilience comes from pricing discipline at the moment of entry, because overpaying is the one mistake you can’t iterate your way out of. It comes from grounding your thesis in industry demand rather than model novelty.

It comes from helping companies build enterprise-grade trust through reliability, safety, and compliance, which expands the universe of potential buyers when the time comes. And it comes from preparing for multiple paths, whether that’s strategic M&A, growth rounds, or public markets.

Optionality isn’t indecision. It’s architecture, and building it early gives you choices when you need them most.

The Constant

Everything I’ve described in this piece, the tools, the workflows, the speed of diligence, all of that will keep changing. A year from now, the specific tactics will look different again.

But the core of venture capital hasn’t moved, and I don’t think it will. The best investors I know, across every era, share the same trait: they can see where an industry is heading before it’s obvious and they have the patience to act on that conviction when the market is loud and the signal is faint. No tool replicates that and no model shortcuts it.

So if you take one thing from this piece, let it be this: sharpen your tools, but sharpen your judgment faster. The tools are available to everyone. Your judgment isn’t.